Oil storage terminals serve a critical role in the oil and gas value chains, it serves as repository for inventory in the chains. Terminal owners do not own the product being stored and are not directly exposed to commodity-price volatility. However, the demand of oil products will affect the utilization rates and storage fees for short-term contracts as well as renewal of long-term lease.

Oil storage terminals are also capital-intensive and asset-heavy industries, they bear a great responsibility situated at the intersection of operational excellence, safety, environmental concerns, risk management and profitability. Due to business complexity, data sensitive and ownership, most oil terminal operators are still using paper contracts or outdated computer software platforms to keep track their contracts with vendors and customers. This article discusses the key justifications in implementing smart contracts for Oil Storage Terminals.

Table of Contents

Concept of Smart Contracts

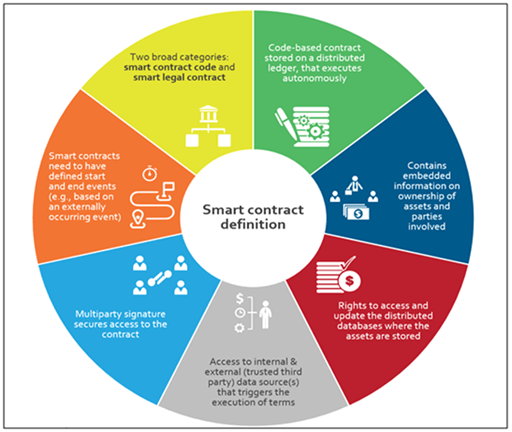

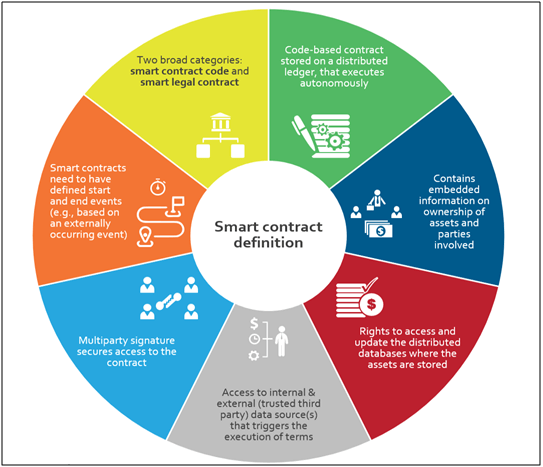

Smart contracts are digital contracts, which paperless can be accessed by any technology devices like desktops, laptops, smartphones at anytime and anywhere. Smart contract was first invented in 1994, by a cryptographer named Nick Szabo, who came up with the idea of being able to record contracts in the form of computer codes and they would activate automatically when certain conditions are met. This idea might eventually remove the need for trusted middlemen like lawyers, brokers, bankers, because the smart contracts are self-executed on a trusted network that is completely controlled by computers.

It works when two parties make an agreement/contract in the form of computer code following a simple “if/when…. then…” logic codes statements that run on the blockchain. Blockchain will process and executes the contract when predetermined conditions have been met and verified, and updated when the contract is completed. Contract cannot be changed, and only parties who been granted permission can see the results. In smart contract, many regulations can be included as needed to enable contract parties to complete tasks satisfactorily. While establishing “terms and conditions”, contract parties must determine how agreements and their data are represented on the blockchain, to agree on the “if/when… then…” rules governing these agreements. They also explore all possible exceptions, and define the framework of the solution to resolve disputes.

Blockchain is essentially a digital ledger, equipped with both decentralized and distributed technologies, and these two elements lead to great security platform for smart contracts. Blockchain technology can integrate with other technologies like IoT, Artificial Intelligence (AI) to make smart contract “smarter”, transparent, with high level of security.

{kind=link}

Smart Contracts Enhance Security and Data-Backups

Through advanced cryptography techniques, sensitive information, and other critical document records are encrypted, which makes them very hard to hack. If hackers want to alter the information in a contract, they would need to hack more than 50% of the nodes on the blockchain. Smart contracts are more secure due to its decentralized structure, each record is connected to the previous and subsequent records on a distributed ledger. This means no one can control or have the ownership of the information, because the blockchain database are ran by many computers (called, “nodes”) the information are “distributed” everywhere, and the true and untampered version is not located in one location. Hackers have to alter the entire chain to change a single record. All the contracts stored on blockchain are duplicated multiple times; thus, originals can be restored in the event of any data loss.

Blockchain is a network of computers storing the data, verification of information is more robust. As every transaction is linked together, creating a more trustworthy string of information, because there is no authority that ‘owns’ the data, there is zero chance of that data can be manipulated in one way or another to benefit any contract parties. This transaction will be recorded in the blockchain and can be viewed at any time. Smart Contract leveraged to AI employ Machine Learning, Robotic Process Automation, Natural Language Processing (NLP), and Text Analytics which transforms contracts into driving force for operational excellence. Automatically identifying and arranging contracts in the contract library.

{kind=link}

Smart Contracts Improve Transparency

Oil storage terminal is at the middle stream of the value chain of oil and gas industry, there are multiple parties involved in operation. There is a lack of trust and transparency between these stakeholders, it is because lack of visibility of data, and legal disputes and settlement delays. This resulted stakeholders act cautiously and spend significant time and money on intermediaries while finalizing agreements. Using smart contract, allows to bring all these stakeholders onto a single platform for enhanced visibility. Majority of the operations can be automated and integrity of data will be maintained throughout the supply chain.

In cases where the contract can be observed publicly, smart contracts can improve this by eliminating intermediaries. These contracts establish trust and transparency between the two parties through the use of blockchain technology. They make it possible to create constant and accessible contracts. Organizations can use smart contracts for its accurate and transparent data recording. Advanced analytics and data-driven optimization are leading to better insights, allowing for increased cross-domain value-chain interactions. In cases that terms and conditions of the agreement can be complied with publicly and digitally, Smart contracts can replace intermediary agreements. It enables uniform financial data-keeping across organization which eliminate the need to exchange other documents such as invoice images. Financial reporting and the integrity of data been improved and market stability also increased.

{kind=link}

Smart Contracts Improve Efficiency and Cost Saving

Oil storage terminal invest time and manpower to ensure all documents are in place and accessible to all stakeholders. This includes contracts, compliance documents, audits, and associated paperwork, however it creates the potential for human errors. Manual contracting process easily lose track of your edits combined with the hassle of saving numerous versions. Mistakes are human, and contracts that only humans deal may have many mistakes. Smart contract process saved all these problems and avoid having bad contract or a complex legal issue because smart contracts can be digitized and automated. There is no need to process files and no need to spend time reconciling errors that are usually caused by manually filling in documents.

The full content is only visible to SIPMM members

Already a member? Please Login to continue reading.

References

Andrew Bruce. (2020). “E&P Digital Solutions: Blockchain Smart Contracts Can Address Industry Pain”. Retrieved from https://www.hartenergy.com/exclusives/ep-digital-solutions-blockchain-smart-contracts-can-address-industry-pain-188315, accessed 04/04/2021.

Cem Dilmegani. (2021). “Smart Contract in 2021: What it is & Why it matters ?”. Retrieved from https://research.aimultiple.com/smart-contracts/, accessed 10/04/2021.

Kalyar Thiri Maung, ADPSM. (2020). “AI Technology Digital Procurement”. Retrieved from SIPMM : https://publication.sipmm.edu.sg/ai-technologies-digital-procurement/, accessed 04/04/2021.

Laura M. (2021). “What is a Smart Contract and How does it Work?”. Retrieved from https://www.bitdegree.org/crypto/tutorials/what-is-a-smart-contract, accessed 10/04/2021.

Nitish Singh. (2020). “How Contract Management Solutions And Blockchain Work Together”. Retrieved from: https://101blockchains.com/contract-management-solutions-and-blockchain/#prettyPhoto, accessed 04/04/2021.

Tai Cheoh Wei, GDPM. (2019). “Blockchain Technology for the Construction Sector”. Retrieved from SIPMM : https://publication.sipmm.edu.sg/blockchain-technology-construction-sector/, accessed 04/04/2021.

Tea Min Lyn, GDSCM. (2019). “Five Application of Blockchain Technology For a Digital Supply Chain”. Retrieved from SIPMM: https://publication.sipmm.edu.sg/five-applications-blockchain-technology-digital-supply-chain/, accessed 21/06/2019.